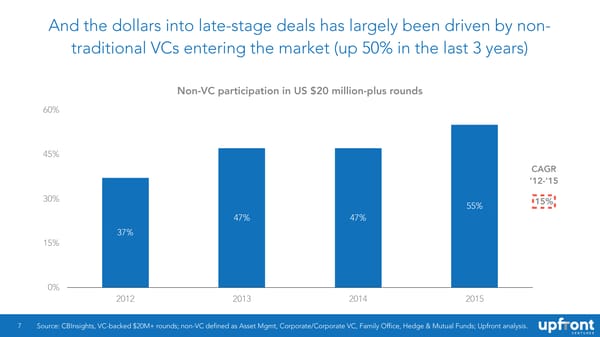

And the dollars into late-stage deals has largely been driven by non- traditional VCs entering the market (up 50% in the last 3 years) Non-VC participation in US $20 million-plus rounds 60% 45% CAGR ’12-’15 30% 55% 15% 47% 47% 37% 15% 0% 2012 2013 2014 2015 7 Source: CBInsights, VC-backed $20M+ rounds; non-VC defined as Asset Mgmt, Corporate/Corporate VC, Family Office, Hedge & Mutual Funds; Upfront analysis.

Bubble? What Bubble? How It's Different This Time. And How It Most Certainly Isn't Page 6 Page 8

Bubble? What Bubble? How It's Different This Time. And How It Most Certainly Isn't Page 6 Page 8